World Bank releases its Global Economic Prospects report on 10 January 2017.

Regional outlook: East Asia and Pacific

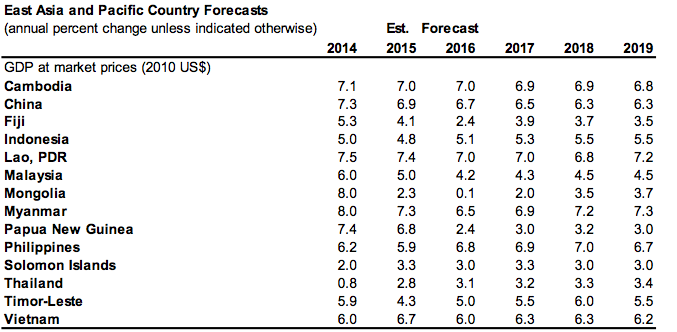

Growth in the East Asia and Pacific region slowed to an estimated 6.3 percent in 2016, in line with expectations, reflecting the gradual deceleration of China. Excluding China, the region grew at a 4.8 percent pace, as a modest acceleration in commodity importers was offset by weaker growth in commodity exporters. Strong domestic spending, supported by generally benign financing conditions for most of 2016, largely counterbalanced weak export growth. Narrowing domestic and external imbalances and stronger policy buffers, coupled with solid growth, helped improve resilience to external headwinds.

Growth in the rest of the region except China was close to its long-term average as robust domestic demand countered weaker external demand. Low and declining inflation enabled central banks in the region to ease or maintain accommodative monetary policy stances last year. Growth picked up in commodity importers, led by the Philippines and Thailand. Activity softened among commodity exporters, including Lao People’s Democratic Republic, Malaysia, Myanmar, and eased considerably in Mongolia and Papua New Guinea, where adjustment needs were significant. Financial markets experienced an uptick in volatility toward the end of the year amid heightened policy uncertainty in the United States.

OUTLOOK

Growth in the East Asia and Pacific region is projected to ease to 6.2 percent in 2017 as slowing growth in China is moderated by a pickup in the rest of the region. Output in China is anticipated to slow to 6.5 percent in the year. Macroeconomic policies are expected to support key domestic drivers of growth despite softness of external demand and overcapacity in some sectors. Excluding China, growth in the region is seen advancing at a more rapid 5 percent rate in 2017.

Growth among commodity exporting economies in the region is forecast to accelerate. The growth outlook has deteriorated in several small commodity exporters, such as Mongolia and Papua New Guinea, where the terms-of-trade shock has exacerbated domestic vulnerabilities.

RISKS

Risks have tilted further to the downside since mid-2016 and include heightened policy uncertainty in advanced economies (Europe and the United States) amid a rise in support for trade protection. Financial market disruption and weak growth in advanced economies would pose further risks to growth. Rising political opposition to trade has contributed to a post-crisis high in new trade restrictions in the past year. The imposition of trade barriers by major trading partners would disproportionately affect the relatively more open economies of East Asia and Pacific.

An unexpected deceleration of major economies in the region or weaker-than-expected global trade would dampen growth in the region, and a faster-than-expected slowdown in China would have sizable regional spillovers.

Similarly, an adverse reaction to the U.S. Federal Reserve’s anticipated rise in interest rates or an increase in global risk aversion could also slow growth. The large, financially integrated economies of the region with sizable external, foreign-currency denominated, and/or short-term debt—such as Indonesia, Malaysia and, to a lesser degree, Thailand—would be most exposed.

World Bank releases its Global Economic Prospects report on 10 January 2017.

Regional outlook: East Asia and Pacific

Growth in the East Asia and Pacific region slowed to an estimated 6.3 percent in 2016, in line with expectations, reflecting the gradual deceleration of China. Excluding China, the region grew at a 4.8 percent pace, as a modest acceleration in commodity importers was offset by weaker growth in commodity exporters. Strong domestic spending, supported by generally benign financing conditions for most of 2016, largely counterbalanced weak export growth. Narrowing domestic and external imbalances and stronger policy buffers, coupled with solid growth, helped improve resilience to external headwinds.

Growth in the rest of the region except China was close to its long-term average as robust domestic demand countered weaker external demand. Low and declining inflation enabled central banks in the region to ease or maintain accommodative monetary policy stances last year. Growth picked up in commodity importers, led by the Philippines and Thailand. Activity softened among commodity exporters, including Lao People’s Democratic Republic, Malaysia, Myanmar, and eased considerably in Mongolia and Papua New Guinea, where adjustment needs were significant. Financial markets experienced an uptick in volatility toward the end of the year amid heightened policy uncertainty in the United States.

OUTLOOK

Growth in the East Asia and Pacific region is projected to ease to 6.2 percent in 2017 as slowing growth in China is moderated by a pickup in the rest of the region. Output in China is anticipated to slow to 6.5 percent in the year. Macroeconomic policies are expected to support key domestic drivers of growth despite softness of external demand and overcapacity in some sectors. Excluding China, growth in the region is seen advancing at a more rapid 5 percent rate in 2017.

Growth among commodity exporting economies in the region is forecast to accelerate. The growth outlook has deteriorated in several small commodity exporters, such as Mongolia and Papua New Guinea, where the terms-of-trade shock has exacerbated domestic vulnerabilities.

RISKS

Risks have tilted further to the downside since mid-2016 and include heightened policy uncertainty in advanced economies (Europe and the United States) amid a rise in support for trade protection. Financial market disruption and weak growth in advanced economies would pose further risks to growth. Rising political opposition to trade has contributed to a post-crisis high in new trade restrictions in the past year. The imposition of trade barriers by major trading partners would disproportionately affect the relatively more open economies of East Asia and Pacific.

An unexpected deceleration of major economies in the region or weaker-than-expected global trade would dampen growth in the region, and a faster-than-expected slowdown in China would have sizable regional spillovers.

Similarly, an adverse reaction to the U.S. Federal Reserve’s anticipated rise in interest rates or an increase in global risk aversion could also slow growth. The large, financially integrated economies of the region with sizable external, foreign-currency denominated, and/or short-term debt—such as Indonesia, Malaysia and, to a lesser degree, Thailand—would be most exposed.